-

1. I am an existing ElderShield/ElderShield Supplement policyholder. Do I have to join CareShield Life?

If you are a Singapore Citizen or Permanent Resident born between 1970 and 1979, covered under the ElderShield 400 scheme and did not develop severe disability, you have been auto-enrolled to CareShield Life from 1 December 2021. You can choose to opt out from CareShield Life by 31 December 2023 if you do not wish to join the scheme.

Those who were not auto-enrolled can choose to join CareShield Life.

The Government will provide means-tested premium subsidies and Additional Premium Support to those who join CareShield Life, to ensure that no one who joins the scheme loses coverage due to financial difficulties.

For more information on the types of premium support available, you may refer to this page. For information on your personalised premiums and premium support, you may access the CareShield Life Premium Checker e-Service with your Singpass.

2. If I am born in 1979 or earlier and develop severe disability, can I join CareShield Life?

If you are unable to perform three or more Activities of Daily Living (i.e. have developed severe disability), you will not be eligible to join CareShield Life.

If you are insured under ElderShield and have not made a claim yet, you may wish to claim from ElderShield instead. Depending on the plan you have, ElderShield provides monthly cash payouts of $300 per month for up to 60 months (under ElderShield 300 plan), or $400 per month for up to 72 months (under ElderShield 400 plan).

If you have received all your ElderShield payouts, you may wish to tap on Government subsidies and various Government assistance schemes (such as the Home Caregiving Grant, ElderFund) for assistance. You may also approach the Medical Social Workers at the health institution you are seeking medical treatment from or your nearest Social Service Office (SSO). For more information on MediFund or ComCare, please visit https://www.moh.gov.sg/managing-expenses/schemes-and-subsidies/medifund or http://www.msf.gov.sg/comcare.

3. I am an existing ElderShield insured. If I am eligible for ElderShield claims, should I claim from ElderShield or join CareShield Life?

If you are unable to perform three or more Activities of Daily Living (i.e. have developed severe disability), and is an ElderShield insured, you should apply to claim under ElderShield so that you can receive your monthly claim payouts in a timely manner.

You will not be eligible for CareShield Life if you have developed severe disability.

4. I am born in 1979 or earlier. Will I have to pay extra premiums if I join CareShield Life with pre-existing medical conditions?

If you are born in 1979 or earlier and have pre-existing medical conditions, you can choose to join CareShield Life if you do not develop severe disability. You will not need to pay additional premiums for pre-existing medical conditions.

You may wish to refer to the CareShield Life Premium Checker e-Service to view your premium details and premium support.

5. Why is universal coverage not extended to those born in 1979 or earlier?

Universal coverage is not extended to those born in 1979 or earlier as this is a diverse group - some may have previously opted out of ElderShield, or decided not to upgrade to ElderShield. Others could have bought Supplements or insurance plans. Those born in 1979 or earlier would also likely face higher entry premiums as they have fewer years to spread their premium payment over. The prevalence of those who already have severe disability in the older cohorts is also much higher, which would make it harder to cover everyone while still keeping premiums affordable. Hence, universal coverage is not extended to those born in 1979 or earlier.

Those who are born in 1979 or earlier and who already have severe disability will not be able to join CareShield Life. The Government will help them through other ways e.g. Government subsidies and other Government schemes such as the Seniors’ Mobility and Enabling Fund. They can also tap on ElderFund and their MediSave savings.

Government-funded safety nets such as MediFund, ComCare can also provide further assistance to Singaporeans who are unable to pay for their care even after Government subsidies and other means of support.

6. Should I opt out of ElderShield if I would like to join CareShield Life?

There is no need to opt out of ElderShield. Your existing ElderShield cover will be upgraded to CareShield Life and the premiums paid for ElderShield will be taken into account.

Simply access the Application to join CareShield Life e-Service using your Singpass and we will notify you on the outcome of your upgrade.

7. I am born in 1979 or earlier. Will ElderShield 300/400 insureds receive subsidies or an incentive as well since there were no incentives in 2002/2007 when ElderShield 300 and 400 were introduced respectively?

CareShield Life premium subsidies and incentives will be extended to Singaporeans (including those on ElderShield 300/400 today) if they join CareShield Life, as these are intended to support the increased benefits under CareShield Life and ensure that CareShield Life premiums remain affordable.

8. I have opted out from ElderShield. Can I join CareShield Life?

You can join CareShield Life if you are a Singapore Citizen or Permanent Resident born in 1979 or earlier and do not have severe disability.

If you wish to join CareShield Life, you may access the Application to join CareShield Life e-Service and log in using your Singpass to complete the application. Some applicants may need to undergo a disability assessment. You will be informed if a disability assessment is required.

9. I am born in 1979 or earlier. If I paid ESH300/400 premiums previously but my policy lapsed due to non-payment of premiums, how will my CareShield Life premiums be affected?

As your ElderShield 300/400 policies have lapsed, you are no longer covered under ElderShield 300/400. Your premiums for CareShield Life will be based on the premiums for an uninsured individual.

Those who need assistance with their premium payment after subsidies and incentives will receive Additional Premium Support, and no one who joins CareShield Life will lose coverage due to financial difficulties.

10. I am born in 1979 or earlier. If I currently have severe disability but subsequently recover, can I join CareShield Life?

If you have recovered from your severe disability, you can choose to join CareShield Life. You may be required to go for a disability assessment to determine your eligibility.

11. If I was previously claiming from ElderShield, but have recovered from my severe disability, can I join CareShield Life?

If you previously claimed from ElderShield but have since recovered, you can choose to join CareShield Life. You may have to go for a disability assessment.

12. Will I receive any premium subsidies as an ElderShield 300/400 insured if I upgrade to CareShield Life?

If you are an ElderShield insured, you can receive CareShield Life premium subsidies if you upgrade to CareShield Life. CareShield Life is a new scheme, and these subsidies will ensure that the premiums remain affordable even as the new scheme offers better protection and benefits.

13. If I am currently on ElderShield 300/400 and choose to upgrade to CareShield Life, can I opt out or downgrade back to ElderShield 300/400 subsequently?

If you are a Singapore Citizen or Permanent Resident born between 1970 and 1979, you will be automatically enrolled in CareShield Life from 1 December 2021, if you are currently covered under the ElderShield 400 scheme and do not develop severe disability at the point of auto-enrolment. You can opt out of CareShield Life by 31 December 2023 if you do not wish to join the scheme and you will automatically be placed back onto your ElderShield 400 scheme.

Those who are not auto-enrolled can choose to join CareShield Life. If you are an ElderShield insured in this group, you will have a 60-day free-look period from the commencement of your CareShield Life coverage, for you to consider your decision. If you choose to opt out, you will be given a full premium refund and automatically be placed back onto your original ElderShield 300/400 scheme.

You will not be able to opt out from the scheme after the applicable opt-out/free-look periods.

14. Should I upgrade to/join CareShield Life?

The Government encourages Singapore Citizens and Permanent Residents born in 1979 or earlier without severe disability to consider joining CareShield Life for basic lifetime financial protection for long-term care. CareShield Life provides monthly cash payout in the event of severe disability, for as long as you are unable to do three or more Activities of Daily Living (ADLs).

The Government also provides support to help make premiums affordable.

15. Will I get higher subsidies if I am of an older age since my CareShield Life premiums will be higher?

If you are born in 1979 or earlier, you will receive means-tested subsidies of up to 30% on your base premiums for CareShield Life. Given that premiums increase with age, the annual subsidies for older Singaporeans will also be higher to offset the higher annual premiums.

Those who need more assistance with their premium payment after subsidies will receive Additional Premium Support.

For more information on the types of premium support available, you may refer to this page. For information on your personalised premiums and premium support, you may access the CareShield Life Premium Checker e-Service with your Singpass.

16. I am born in 1979 or earlier. Can I opt out from the CareShield Life scheme after joining (e.g. if I cannot afford the premiums)?

To make joining CareShield Life more convenient, you have been auto-enrolled from 1 December 2021, if you are a Singapore Citizen or Permanent Resident born between 1970 and 1979, covered under the ElderShield 400 scheme and did not develop severe disability at the point of auto-enrolment. You can choose to opt out by 31 December 2023 if you do not wish to join the scheme.

Those who are not auto-enrolled can choose to join CareShield Life. If you are in this group, you will have a 60-day free-look period from the commencement of your CareShield Life coverage, for you to consider your decision.

The Government will provide means-tested premium subsidies and Additional Premium Support to those who join CareShield Life, to ensure that no one who joins the scheme loses coverage due to financial difficulties. For this reason, after the applicable free-look periods, you will not be able to opt out from the scheme.

For more information on the types of premium support available, you may refer to this page. For information on your personalised premiums and premium support, you may access the CareShield Life Premium Checker e-Service with your Singpass.

If you are a foreigner who become a Singapore Citizen or a Permanent Resident from 1 October 2020 onwards, are born in 1979 or earlier and do not develop severe disability, CareShield Life will be mandatory for you.

17. If I have finished claiming my ElderShield 300/400 payouts, can I still join CareShield Life?

You can choose to join CareShield Life but you may be required to undergo a disability assessment. You will not be eligible to join CareShield Life if you are unable to do three or more Activities of Daily Living (ADLs).

However, you can tap on Government subsidies and various Government assistance schemes such as Home Caregiving Grant and ElderFund, and MediSave Care to complement your personal savings and family support, in meeting your long-term care needs. Government assistance schemes such as the Seniors' Mobility and Enabling Fund can also help defray the cost of consumables and assistive devices.

18. The current ElderShield scheme has a maximum entry age of 64 years old. Can I join CareShield Life if I am older?

There is no maximum entry age for CareShield Life.

However, as premiums increase with age, you are advised to use the Premium Checker using your Singpass to check your personalised premium payable before applying to join CareShield Life.

19. I am born in 1979 or earlier and did not qualify to join ElderShield previously. Am I eligible to join CareShield Life now?

You can choose to join CareShield Life if you are a Singapore Citizen or Permanent Resident born in 1979 or earlier and do not have severe disability. Some applicants may need to undergo a disability assessment. You will be informed if a disability assessment is required.

20. Can I join both CareShield Life and ElderShield to get double the protection?

You will not be able to be on both CareShield Life and ElderShield.

However, upgrading to CareShield Life will not affect your ElderShield Supplement plan if you already have one. If you are currently covered under ElderShield, you can upgrade to CareShield Life for higher and lifetime payouts. Your ElderShield coverage will be terminated upon joining CareShield Life. For more coverage, you can also purchase Supplement plans from private insurers.

21. I am born in 1979 or earlier, and am not enrolled in ElderShield. Am I eligible for CareShield Life?

You can join CareShield Life if you are a Singapore Citizen or Permanent Resident born in 1979 or earlier and do not develop severe disability.

22. What will happen to my current ElderShield and Supplement plans after CareShield Life is launched?

The launch of CareShield life will not affect your existing ElderShield and supplement plans.

However, you are encouraged to consider upgrading your ElderShield to CareShield Life if you do not have severe disability. If you choose to upgrade to CareShield Life, the ElderShield premiums that you have paid will be taken into account when computing your CareShield Life premiums, resulting in lower CareShield Life premiums.

The Supplements will also work with CareShield Life cover and do not need to be terminated.

23. I am born in 1979 or earlier. Do I need to back pay premiums from age 30 to join CareShield Life?

ElderShield premiums that ElderShield insureds have paid will be taken into account when computing their CareShield Life premiums. Insureds do not need to back pay for CareShield Life coverage starting from 30; they will only be paying for coverage going forward.

However, CareShield Life's annual premiums for older insureds will still be higher than those of younger insureds, as they have less years to spread their premium payment over.

24. Why is the Government auto-enrolling ElderShield 400 insureds who are born between 1970 to 1979 to CareShield Life?

It was to make it more convenient for Singapore Citizens and Permanent Residents to join CareShield Life. If you were auto-enrolled and do not wish to join the scheme, you can opt out by accessing the Opt-out of CareShield Life e-Service and log in using Singpass to complete the application by 31 December 2023.

25. How do the CareShield Life premiums and monthly payouts compare against Supplements and other private long-term care insurance plans?

Supplement premiums are not directly comparable as there are inherent differences in the product design of CareShield Life, Supplements and other private long-term care products:

• Currently, there are no Supplement plans with increasing payouts, although there are Supplement plans that have a higher payout quantum and no cap on payout duration, similar to CareShield Life.

• Supplements generally have premium schedules designed to keep annual premiums lower e.g. some of them allow premiums to be paid up to age 80, 100 or over the insured’s lifetime while CareShield Life only requires premiums to be paid up to age 67. Some Supplements offer additional benefits, such as death benefit, lump sum benefit upon claim or payouts upon not being able to perform at least two out of the six Activities of Daily Living (ADLs), which CareShield Life does not provide.As part of CareShield Life, the Government will be providing several premium support measures for those born in 1979 or earlier, including means-tested premium subsidies, participation incentives, and Additional Premium Support for those who are unable to pay their CareShield Life premiums even after premium subsidies. No one will lose coverage due to financial difficulties.

In addition, CareShield Life will be administered by the Government on a not-for-profit basis. Government administration will enable the provision of premium support for lower- and middle-income Singaporeans and offer more flexibility for future scheme enhancements.

26. I am born in 1979 or earlier. Will I be able to join or upgrade to CareShield Life?

You can join or upgrade to CareShield Life if you are a Singapore Citizen or Permanent Resident born in 1979 or earlier and do not have severe disability.

For more information on the types of premium support available, you may refer to this page. For information on your personalised premiums and premium support, you may access the CareShield Life Premium Checker e-Service with your Singpass.

27. Do I have to undergo a disability assessment before joining CareShield Life?

You may be required to undergo a disability assessment prior to joining CareShield Life. Should you be required to attend a disability assessment, you will receive a letter with instructions on how to do so.

28. What is the difference between CareShield Life, ElderShield, MediShield Life, CPF LIFE, ElderFund, Community Health Assist Scheme (CHAS), Home Caregiving Grant (HCG) , Pioneer Generation Disability Assistance Scheme (PioneerDAS) and Interim Disability Assistance Programme for the Elderly (IDAPE)?

CareShield Life, ElderShield, MediShield Life, CPF LIFE, CHAS, HCG, PioneerDAS, ElderFund and IDAPE are schemes that help Singaporeans with different types of healthcare and retirement expenses.

CareShield Life and ElderShield are long-term care insurance schemes that will provide Singapore Citizens and Permanent Residents with some financial protection should one develop severe disability (i.e. unable to perform at least three or more of the six Activities of Daily Living (ADLs)), especially in old age.

For CareShield Life, Singapore Citizens or Permanent Residents born in 1980 or later will be automatically covered under CareShield Life on 1 October 2020, or when they turn 30, whichever is later. Singapore Citizens or Permanent Residents born in 1979 or earlier can choose to join CareShield Life if they do not develop severe disability. CareShield Life insureds can receive monthly payouts for as long as they are unable to do three or more ADLs. Monthly payout is $662 in 2025 and increases annually until age 67 or when a successful claim is made, whichever is earlier.

For ElderShield, eligible Singapore Citizens and Permanent Residents who had a MediSave Account when they turned 40 years old in 2019 or earlier were automatically covered under ElderShield. Depending on the plan you have, in the event of severe disability, ElderShield provides monthly cash payouts of $300 per month for up to 60 months (under ElderShield 300 plan), or $400 per month for up to 72 months (under ElderShield 400 plan).

MediShield Life is a basic healthcare insurance plan that protects all Singapore Citizens and Permanent Residents against large medical bills for life.

CPF LIFE is the national longevity insurance annuity scheme, which insures Singapore Citizens and Permanent Residents against the risk of outliving their retirement savings. Under CPF LIFE, members will receive a monthly payout from their payout eligibility age, for as long as they live.

Community Health Assist Scheme (CHAS) enables all Singapore Citizens, including Pioneer Generation (PG) and Merdeka Generation (MG) cardholders, to receive subsidies for medical and/or dental care at participating General Practitioner (GP) and dental clinics. CHAS was implemented to allow CHAS cardholders to enjoy more subsidies at Specialist Outpatient Clinics (SOCs) in public hospitals when referred by CHAS-partnered clinics or polyclinics.

Home Caregiving Grant (HCG) is a monthly cash grant of $200 to support families caring for loved ones with permanent moderate disability (i.e. always require some assistance with at least three Activities of Daily Living (ADLs)) who reside in the community. The HCG can be used to defray caregiving expenses, such as the cost of eldercare and services in the community or hiring of a foreign domestic worker.

Pioneer Generation Disability Assistance Scheme (PioneerDAS) offers life-long monthly cash assistance of $100 to Pioneers with permanent moderate disability (i.e. always require some assistance with at least three ADLs). Applicants must be a Pioneer to be eligible.

Interim Disability Assistance Programme for the Elderly (IDAPE) offers a monthly cash assistance of up to $250 to needy elderly Singapore Citizens living in Singapore who are needy, have developed severe disability and are unable to join ElderShield when it was launched in 2002 either because they had exceeded the maximum entry age or had pre-existing disabilities.

ElderFund is a discretionary government assistance scheme providing monthly cash assistance of up to $250 to lower-income Singapore Citizens, aged 30 and above, who have developed severe disability and are not able to benefit from CareShield Life, ElderShield and Interim Disability Assistance Programme for the Elderly (IDAPE), and have low MediSave balances and inadequate personal savings to meet their long-term care needs.

29. Can I opt-out from CareShield Life?

Please select the age group you belong to.

If you are a Singapore Citizen or Permanent Resident born in 1980 or later, CareShield Life will be universal and mandatory for you. You will not be able to opt out.

CareShield Life is a long-term care insurance which provides financial protection against long-term care costs of Singaporeans in the event of severe disability. CareShield Life will provide you with better protection and assurance for basic long-term care needs with:

- 1. Lifetime cash payouts, for as long as the insured is unable to do three or more Activities of Daily Living (ADLs);

- 2. Increasing monthly payouts, at $662/month in 2025 and increases annually until age 67 or when a successful claim is made, whichever is earlier;

- 3. Government subsidies to make it affordable, with no one losing coverage if they cannot pay premiums;

- 4. Premiums can be fully paid by MediSave.

If you are a Singapore Citizen or Permanent Resident born between 1970 and 1979, who was covered under the ElderShield 400 scheme, you have been automatically enrolled in CareShield Life from 1 December 2021. A welcome notification package would have been sent to you in November 2021, informing you of your coverage and that after the end of the free-look-period (FLP) on 31 December 2023, you would continue to be covered under the scheme. We are unable to accede to opt-out requests for members whose FLP had ended on 31 December 2023.

CareShield Life offers lifelong protection against the costs of long-term care in the event of severe disability. Find out how CareShield Life protects you for life.

If you were not auto-enrolled and had chosen to join CareShield Life, you may opt-out of CareShield Life by accessing the Opt-out of CareShield Life e-Service. Log in using your Singpass to complete the application Please complete the application within the 60 days free-look period from your CareShield Life cover commencement date. If you were covered under ElderShield prior to your joining of CareShield Life, your ElderShield will be automatically reinstated after you have opted-out of CareShield Life, subject to successful collection of ElderShield premiums (if any).

You will not be able to opt-out from CareShield Life after the 60 days free-look period.

If you are a foreigner who become a Singapore Citizen or a Permanent Resident from 1 October 2020 onwards, is born in 1979 or earlier and have not developed severe disability, CareShield Life will be mandatory for you.

30. I do not have a CPF account. Can I still join CareShield Life?

If you do not have a CPF account, you will still be invited to join the scheme. You can make your first premium payment via the following methods:

(1) Opening a CPF account by making a top-up to your MediSave Account

(2) A family member* can apply to take over as your premium payer using his/her MediSave savings. To do so, he/she may visit the Change Premium Payer e-Service and log in using his/her own Singpass to complete the “Change Premium Payer” transaction.*Family member refers to the Insured's spouse, parents, children, siblings or grandchildren.

31. I am born in 1979 or earlier. If I join CareShield Life, will I get premium rebates?

An independent council has been set up to regularly review and recommend premium and payout adjustments for CareShield Life, in accordance with an actuarially sound adjustment framework.

Should the amount of claims be lower than expected, the council could recommend adjustments to future payouts and premiums (e.g. to reduce the rate of premium increases, or even lower the premiums). Conversely, if the amount of claims is higher than expected, the council could recommend adjustments (e.g. increase the rate of premium increases) to make the scheme more sustainable. A premium rebate is one possible mechanism within this framework.

32. I have submitted my application to join CareShield Life and received a letter to attend a disability review. How do I go about it?

Please contact an MOH-accredited assessor to schedule your disability review. Your letter will include instructions on how to attend a disability assessment.

If you need further assistance, please contact AIC at 1800 650 6060 or submit an enquiry via “My Correspondences” at https://efinance.aic.sg with your Singpass Login.

33. I have already paid for ElderShield premiums for this year. Will I get any refund if I apply to join CareShield Life?

The ElderShield premiums will be refunded if you join CareShield Life and your CareShield Life commencement date is in the same year as your ElderShield policy renewal.

For example, if you paid ElderShield Premiums in September 2021 (for your ElderShield policy renewal in 2021), and later joined CareShield Life in December 2021, the ElderShield premiums you have paid in September 2021 will be refunded to you.

The refund of ElderShield premiums (if any) will take place upon collection of the first CareShield Life premium.

34. I have applied to join CareShield Life online. Where do I check for my application status?

You may view the status of your application via the My Transactions e-Service (Singpass login is required).

35. I have applied to join CareShield Life online. When would I be informed of my application outcome?

We will notify you on the outcome in approximately seven working days if your application has been approved, unsuccessful or pending assessment. You will be notified via the e-mail address that you have registered with a government agency (e.g. Singpass). If there is no e-mail address registered, an SMS will be sent instead.

A letter will only be sent out if both e-mail address and mobile number are unavailable.

36. I do not have Singpass. Can I apply to join CareShield Life via a hardcopy form?

Please apply for Singpass via the Singpass website. Alternatively you may contact the Singpass Helpdesk at support@singpass.gov.sg or 65 6643 0555.

Thereafter, you can apply to join CareShield Life with your Singpass

37. I have applied for CareShield Life and my application has been approved. When will my premiums be deducted?

Your CareShield Life premium will be automatically deducted from your or your payer’s MediSave within two months from your policy start date. Please ensure you have sufficient funds in your MediSave for CareShield Life premium payment.

38. I have applied for CareShield Life and my application has been approved. Why is the coverage status reflected as ‘Waiting for Cover’ on My Policy e-Service?

Coverage status will be reflected as 'Active' only after successful premium deduction (about two months from your approved date).

However, please be assured that you will still be eligible for claims while your coverage status is 'Waiting for Cover'.

39. I have applied for CareShield Life and my application has been approved. Why does it not show up on the Healthcare dashboard – “Long-term care insurance” section?

The information will be displayed after successful premium deduction.

Nevertheless, please be assured that once your application has been approved, that would be your policy start date and you will be eligible to claim if the onset of severe disability falls on or after that date.

40. My CareShield Life coverage status on the My Policy e-Service is reflected as ‘Waiting for Cover’. Will I be able to claim from CareShield Life?

As your CareShield Life application has been approved, you will be eligible to claim if the onset of severe disability falls on or after your CareShield Life policy start date. This applies even if the premiums have not been deducted.

Should you wish to claim from CareShield Life, you can submit your application via the Agency for Integrated Care (AIC) eServices for Financing Schemes (eFASS) Application Portal using your Singpass.

41. Why are Government subsidies provided for CareShield Life and not for ElderShield?

Government subsidies are provided for CareShield Life as it is a mandatory scheme for Singapore Citizens and Permanent Residents born in 1980 or after, unlike ElderShield which is optional.

While CareShield Life is also optional for those born before 1979, they would not be able to cancel their CareShield Life cover after the 60-days free-look period. Premium subsidies are provided to help the lower- to middle-income pay their CareShield Life premiums. On the other hand, ElderShield policyholders have the option to opt out or cancel their policy anytime.

42. Why is my participation incentive $0?

Participation Incentives were only extended to Singapore Citizens (SCs) born in 1979 or earlier who joined and were covered under CareShield Life by 31 December 2024. However, both SCs and Permanent Residents (PRs) will be entitled to Government subsidies, if you are from a lower- to middle-income household. PRs enjoy half the applicable subsidies that SCs enjoy.

43. I have applied to opt out of CareShield Life as I belong to the optional group (i.e. born in 1979 or earlier) and the cover is still within my free-look period. When will my application be approved?

Your application to opt out of CareShield Life will be processed after one working day. You will receive a notification once your application has been processed.

You may view the status of your application via My Transactions e-Service (Singpass login is required).

44. I was born in 1979 or earlier and would like to opt out of CareShield Life. When will the premiums be refunded to my MediSave if I opt out?

You will not be able to opt out from CareShield Life after the applicable opt-out/free-look period. If you choose to opt out of CareShield Life within the applicable opt-out/free-look period, you will be given a full premium refund after one working day. If you were covered by ElderShield prior to your enrolment into CareShield Life, you will be automatically placed back onto your original ElderShield scheme.

You may view the refund made to your MediSave via Transaction History at cpf.gov.sg (Singpass login is required).

45. I am a Singapore Citizen born in 1979 or earlier who joined and was covered under CareShield Life by 31 December 2024. How much CareShield Life participation incentives am I eligible for?

The Total Participation Incentives you are eligible for will be spread equally over 10 years and will be used to offset the annual premium payable in that year.

For Singapore Citizens who joined and were covered under CareShield Life by 31 December 2023:

For Singapore Citizens who joined and were covered under CareShield Life between 1 January 2024 and 31 December 2024:

.png)

You may also access the CareShield Life Premium Checker e-Service with your Singpass for information on your personalised premiums and premium support, which includes the participation incentives you are eligible for.

These Participation Incentives will not apply if you join and are covered under CareShield Life after 31 December 2024.

46. Can I sign up for CareShield Life on behalf of my parent/spouse/sibling?

Your family member’s Singpass will be required to sign up for CareShield Life.

You can guide your family member to use his/her Singpass to apply for CareShield Life by accessing cpf.gov.sg/CSLeServices > Application to join CareShield Life e-Service. Some applicants may need to undergo a disability assessment. Your family member will be informed by Agency for Integrated Care (AIC) if a disability assessment is required, after his/her application.

If they are facing difficulties you can accompany them to the Community Clubs/Centres or CPF Service Centres to sign up.

47. Will I receive the Participation Incentives of up to $3,000 as long as I apply to join by 31 December 2024?

It depends on whether you will be required to undergo a disability assessment as part of the underwriting process.

If you are not required to undergo a disability assessment by the Agency for Integrated Care (AIC) and apply to join CareShield Life using our eService by 31 December 2024, you will be eligible for Participation Incentives of up to $3,000.

If you are required to undergo a disability assessment by AIC and attend your disability assessment after 31 December 2024, you will not be eligible for the Participation Incentives of up to $3,000 as your application will only be approved as per your disability assessment date.

Therefore, you are encouraged to apply to join CareShield Life early if you are planning to do so.

- 1. Lifetime cash payouts, for as long as the insured is unable to do three or more Activities of Daily Living (ADLs);

-

1. What is CareShield Life?

CareShield Life is a long-term care insurance which provides financial protection against long-term care costs of Singaporeans in the event of severe disability. CareShield Life will provide you with better protection and assurance for basic long-term care needs with:

1. Lifetime cash payouts, for as long as the insured is unable to do three or more Activities of Daily Living (ADLs);

2. Increasing monthly payouts, at $662/month in 2025 and increases annually until age 67 or when a successful claim is made, whichever is earlier;

3. Government subsidies to make it affordable, with no one losing coverage if they cannot pay premiums;

4. Premiums can be fully paid by MediSave.

If you are a Singapore Citizen or Permanent Resident born in 1980 or later, you will be automatically covered on 1 October 2020 or when you turn 30, even if you have any pre-existing conditions or have developed severe disability.

2. Is CareShield Life mandatory?

CareShield Life will be universal and mandatory for you if you are a Singapore Citizen or Permanent Resident born in 1980 or later. This will ensure that all Singaporeans, including those who are more vulnerable such as the lower-income group and those with pre-existing severe disabilities, have basic protection for long-term care needs.

A universal scheme allows those with pre-existing disabilities, who will otherwise not be able to enjoy coverage, to be included. If the scheme is optional, vulnerable groups like the low-income may also drop out of the scheme because of an inability to pay. Some low-income insureds do have their ElderShield policies lapse as the years pass as they are not able to make their premium payments.

Including these groups strengthens our social compact and is consistent with our values as an inclusive and caring society. Many Singaporeans who were engaged in earlier focus groups discussions recognised its merit and supported this approach.

Under CareShield Life, the Government will support Singaporeans who are unable to afford their premiums, so that no one will lose their coverage due to financial difficulties.

Please note that if you are a foreigner who become a Singapore Citizen or a Permanent Resident from 1 October 2020 onwards, is born in 1979 or earlier and do not develop severe disability, CareShield Life will be mandatory for you.

3. Why is there a need to start CareShield Life earlier at age 30?

Starting CareShield Life at age 30 allows a longer period for premiums payment to be spread over. A longer duration of premium payment allows insureds to spread premium payment over more years, so as to reduce annual premiums payable. Consequently, insureds will benefit from additional years of coverage starting from age 30.

By the age of 30, most Singaporeans would have started working and many would have worked for a few years. It is also a good time to start planning for their long-term care needs. They would have started contributing to their MediSave, and should be able to cover their CareShield Life premiums without out-of-pocket expenses.

4. I am born in 1990 or later, when will I be notified of my CareShield Life cover?

If you are born after 1990, you will receive a CareShield Life welcome package about two months before your 30th birthday.

5. I am going to be 29 years old when CareShield Life is launched. If I have severe disability, will I be able to join the scheme earlier?

Under CareShield Life, premiums paid by insureds are designed to be risk-pooled within their own generation and used to cover their claims in the event of severe disability.

As there is no risk pool for your cohort when the scheme is launched, your cohort will be covered under CareShield Life when you turn 30 years old, even if you have developed severe disability.

You may refer to Government support schemes specifically for younger Singaporeans who have developed disability and their caregivers (age 65 and below) on the SG Enable's website or speak to SG Enable at 1800-8585-885.

6. Why are Singaporeans not covered by CareShield Life from birth?

The priority of CareShield Life is to provide protection against severe disability during old age, when Singaporeans are most likely to need long-term care.

There are various support schemes for families who need support for their loved ones who are younger than the starting age (of 30) for CareShield Life but have developed severe disability, e.g. subsidies for early intervention programmes under the Ministry of Social and Family Development (MSF), and subsidies for therapy services at KK Hospital and the National University Hospital.

Government-funded safety nets such as MediFund or ComCare can provide further assistance to Singaporeans who are unable to pay for their care even after Government subsidies and other means of support.

7. I am born in 1980 or later and am terminally ill but do not develop severe disability. Can I be exempted from CareShield Life?

As CareShield Life is universal for Singapore Citizens and Permanent Residents born in 1980 or later, there are no exemptions. As long as you are covered under CareShield Life, you can still receive monthly payouts in the event of severe disability.

The Government will support Singaporeans who are unable to afford their premiums, so that no one will lose their coverage due to financial difficulties.

8. I am born in 1980 or later, and I have pre-existing severe disabilities or medical conditions. Do I need to pay additional CareShield Life premiums?

All Singaporean Citizens and Permanent Residents born in 1980 or later, including those with pre-existing severe disabilities, will be able to enjoy benefits under CareShield Life, regardless of your ability to pay premiums. As such, you will not have to pay additional CareShield Life premiums.

As part of collective responsibility, those with pre-existing severe disabilities should contribute one premium to join the scheme. The payment amount is less than the first monthly CareShield Life payout you will receive. Upon joining the scheme, you will continue to receive monthly payouts for as long as you are unable to do three or more Activities of Daily Living (ADLs).

The Government will provide means-tested premium subsidies, and Additional Premium Support to help those who are still unable to afford premiums even after subsidies. Claims will be paid out as long as insureds meet the claims criteria.

9. I am born in 1980 or later. Why should I pay for the inclusion of those with pre-existing disabilities into CareShield Life?

Including those with pre-existing severe disabilities will strengthen collective responsibility and is fundamental to the inclusive and caring society Singaporeans seek to build. Less than 0.1% of Singaporeans aged 30 to 40 are estimated to have pre-existing severe disability. Hence, the cost of covering those with pre-existing severe disability amongst those born in 1980 or later does not have a significant impact on premiums.

10. I am born in 1980 or later and I have pre-existing severe disabilities. Will I need to pay premiums for CareShield Life?

If you are born in 1980 or later, you will be able to enjoy protection under CareShield Life, regardless of your ability to pay premiums, even if you have pre-existing disabilities.

As part of collective responsibility, those with pre-existing disabilities should contribute one premium payment to join the scheme. The payment amount is less than the first monthly CareShield Life payout you will receive. Upon joining the scheme, you will continue to receive monthly payouts for as long as you are unable to do three or more Activities of Daily Living (ADLs).

The Government will provide means-tested premium subsidies, and Additional Premium Support to help those who are still unable to afford premiums even after subsidies. Claims will be paid out as long as insureds meet the claims criteria.

11. If I reside overseas, can I suspend my premium payment for CareShield Life?

CareShield Life will provide monthly cash payouts in the event of severe disability. Today, overseas Singaporeans are able to file ElderShield claims from abroad and receive payouts to support their care costs wherever they may be. This applies even for those who have permanently relocated abroad. This will continue to apply for CareShield Life. Hence, premium payments for overseas Singaporeans cannot be suspended.

12. If I have already bought private insurance plans for disability, will there be duplicative coverage when I join CareShield Life?

There are different private insurance plans on the market. Most cover total and permanent disability or are meant to insure against loss of income when an individual develops disability and is unable to work. As such, private insurance plans typically cease coverage between ages 60 to 70 when most insureds retire. CareShield Life, however, provides lifetime coverage and ensures that an individual will receive coverage even if the individual develops severe disability in their later years.

In addition, unlike private insurance products which cease coverage if insureds are unable to pay the premiums, under CareShield Life, coverage will not cease if an individual is unable to pay premiums due to financial difficulties. The Government will provide premium subsidies and additional premium support.

13. I am born in 1980 or later and have developed severe disability. Can I still benefit from CareShield Life?

CareShield Life will cover all Singapore Citizens and Permanent Residents born in 1980 or later, including those who have pre-existing medical conditions or severe disability. You will be able to benefit from CareShield Life after you are enrolled into CareShield Life on 1 October 2020 or when you turn 30 years old, whichever is later.

14. I am born in 1980 or later. When can I join CareShield Life?

If you are born in 1980 and after, you will be automatically covered by CareShield Life on 1 October 2020 or when you turn 30.

15. What is the difference between CareShield Life, ElderShield, MediShield Life, CPF LIFE, ElderFund, Community Health Assist Scheme (CHAS), Home Caregiving Grant (HCG) , Pioneer Generation Disability Assistance Scheme (PioneerDAS) and Interim Disability Assistance Programme for the Elderly (IDAPE)?

CareShield Life, ElderShield, MediShield Life, CPF LIFE, CHAS, HCG, PioneerDAS, ElderFund and IDAPE are schemes that help Singaporeans with different types of healthcare and retirement expenses.

CareShield Life and ElderShield are long-term care insurance schemes that will provide Singapore Citizens and Permanent Residents with some financial protection should one develop severe disability (i.e. unable to perform at least three or more of the six Activities of Daily Living), especially in old age.

For CareShield Life, Singapore Citizens or Permanent Residents born in 1980 or later will be automatically covered under CareShield Life on 1 October 2020, or when they turn 30, whichever is later. Singapore Citizens or Permanent Residents born in 1979 or earlier can choose to join CareShield Life if they do not develop severe disability. CareShield Life insureds can receive monthly payouts for as long as they are unable to do three or more ADLs. Monthly payout is $662 in 2025 and increases annually until age 67 or when a successful claim is made, whichever is earlier.

For ElderShield, eligible Singapore Citizens and Permanent Residents who had a MediSave Account when they turned 40 years old in 2019 or earlier were automatically covered under ElderShield. Depending on the plan you have, in the event of severe disability, ElderShield provides monthly cash payouts of $300 per month for up to 60 months (under ElderShield 300 plan), or $400 per month for up to 72 months (under ElderShield 400 plan).

MediShield Life is a basic healthcare insurance plan that protects all Singapore Citizens and Permanent Residents against large medical bills for life.

CPF LIFE is the national longevity insurance annuity scheme, which insures Singapore Citizens and Permanent Residents against the risk of outliving their retirement savings. Under CPF LIFE, members will receive a monthly payout from their payout eligibility age, for as long as they live.

Community Health Assist Scheme (CHAS) enables all Singapore Citizens, including Pioneer Generation (PG) and Merdeka Generation (MG) cardholders, to receive subsidies for medical and/or dental care at participating General Practitioner (GP) and dental clinics. CHAS was implemented to allow CHAS cardholders to enjoy more subsidies at Specialist Outpatient Clinics (SOCs) in public hospitals when referred by CHAS-partnered clinics or polyclinics.

Home Caregiving Grant (HCG) is a monthly cash grant of $200 to support families caring for loved ones with permanent moderate disability (i.e. always require some assistance with at least three Activities of Daily Living (ADLs)) who reside in the community. The HCG can be used to defray caregiving expenses, such as the cost of eldercare and services in the community or hiring of a foreign domestic worker.

Pioneer Generation Disability Assistance Scheme (PioneerDAS) offers life-long monthly cash assistance of $100 to Pioneers with permanent moderate disability (i.e. always require some assistance with at least three ADLs). Applicants must be a Pioneer to be eligible.

Interim Disability Assistance Programme for the Elderly (IDAPE) offers a monthly cash assistance of up to $250 to needy elderly Singapore Citizens living in Singapore who are needy, have developed severe disability and are unable to join ElderShield when it was launched in 2002 either because they had exceeded the maximum entry age or had pre-existing disabilities.

ElderFund is a discretionary government assistance scheme providing monthly cash assistance of up to $250 to lower-income Singapore Citizens, aged 30 and above, who have developed severe disability and are not able to benefit from CareShield Life, ElderShield and Interim Disability Assistance Programme for the Elderly (IDAPE), and have low MediSave balances and inadequate personal savings to meet their long-term care needs.

16. How can I find out if I am covered under CareShield Life?

You can log in to My Policy using your Singpass to find out if you are covered under CareShield Life.

17. What happens to an insured’s CareShield Life policy when he/she passes away?

An insured’s CareShield Life policy will be terminated when he/she passes away. Any premiums paid will refunded to the premium payer’s MediSave if the insured passes away within the first 60 days of the first policy year. No premium refund will be made thereafter.

18. Who should I contact if I have enquiries relating to CareShield Life?

For CareShield Life matters, you may contact us at Write to us or 1800 222 3399/+65 6222 3399 (overseas) from Monday to Friday, 8.00 am to 5.30 pm

19. I am born in 1980 or later, when will I be notified of my CareShield Life cover?

If you are born in 1980 or later, you will be automatically covered under CareShield Life on 1 October 2020, or when you turn 30, whichever is later.

If you are born between 1980 and 1990 (i.e. aged 30 to 40 in 2020), you will receive a CareShield Life welcome package informing you of your CareShield Life cover, by 2 September 2020 or up to two months before your 30th birthday, whichever is later. If you are born after 1990 (i.e. aged below 30 in 2020), you will receive a CareShield Life welcome package before you reach age 30.

20. Can I opt-out from CareShield Life?

Please select the age group you belong to.

You selected: I am a Singapore Citizen or Permanent Resident born in 1980 or later

If you are a Singapore Citizen or Permanent Resident born in 1980 or later, CareShield Life will be universal and mandatory for you. You will not be able to opt out.

CareShield Life is a long-term care insurance which provides financial protection against long-term care costs of Singaporeans in the event of severe disability. CareShield Life will provide you with better protection and assurance for basic long-term care needs with:

- 1. Lifetime cash payouts, for as long as the insured is unable to do 3 or more Activities of Daily Living (ADLs);

- 2. Increasing monthly payouts, at $662/month in 2025 and increases annually until age 67 or when a successful claim is made, whichever is earlier;

- 3. Government subsidies to make it affordable, with no one losing coverage if they cannot pay premiums;

- 4. Premiums can be fully paid by MediSave.

If you are a Singapore Citizen or Permanent Resident born between 1970 and 1979, you have been automatically enrolled in CareShield Life from 1 December 2021, if you were covered under the ElderShield 400 scheme and have not developed severe disability at the point of auto-enrolment. You can opt out of CareShield Life by 31 December 2023 if you do not wish to join the scheme.

To opt-out of CareShield Life, you may access the Opt-out of CareShield Life e-Service and log in using Singpass to complete the application by 31 December 2023 if you were auto-enrolled in 2021. Your ElderShield will be automatically reinstated, subject to successful collection of ElderShield premiums (if any). You will not be able to opt-out from CareShield Life after 31 December 2023.

If you were not auto-enrolled and had chosen to join CareShield Life, you may opt-out of CareShield Life by accessing the Opt-out of CareShield Life e-Service. Log in using your Singpass to complete the application Please complete the application within the 60 days free-look period from your CareShield Life cover commencement date. If you were covered under ElderShield prior to your joining of CareShield Life, your ElderShield will be automatically reinstated after you have opted-out of CareShield Life, subject to successful collection of ElderShield premiums (if any).

You will not be able to opt-out from CareShield Life after the 60 days free-look period.

If you are a foreigner who become a Singapore Citizen or a Permanent Resident from 1 October 2020 onwards, is born in 1979 or earlier and have not developed severe disability, CareShield Life will be mandatory for you.

21. What happens to an insured’s CareShield Life policy when he/she is no longer a Singapore Citizen or Permanent Resident?

The insured’s CareShield Life policy will be automatically terminated and any premiums paid will be refunded to the premium payer’s MediSave if it is within the first 60 days of the first policy year. No premium refund will be made thereafter.

22. I am born in 1980 or later, who can be covered under CareShield Life?

If you are born in 1980 or later, you will be automatically covered under CareShield Life from 1 October 2020, or when you turn 30, whichever is later.

23. When do I have to pay for my CareShield Life premiums?

Your CareShield Life premium is payable annually. The premium payable will be automatically deducted from your or your premium payer’s MediSave within one month from your policy anniversary. You can refer to the My Policy e-Service to check if you have any premiums payable.

- 1. Lifetime cash payouts, for as long as the insured is unable to do 3 or more Activities of Daily Living (ADLs);

-

1. What is the monthly payout amount for CareShield Life?

A successful CareShield Life claimant can receive monthly payouts for the entire duration of severe disability (i.e. for as long as he/she develops severe disability) and continues to be insured under CareShield Life. This is meant to provide better protection against the uncertainty of long-term care costs.

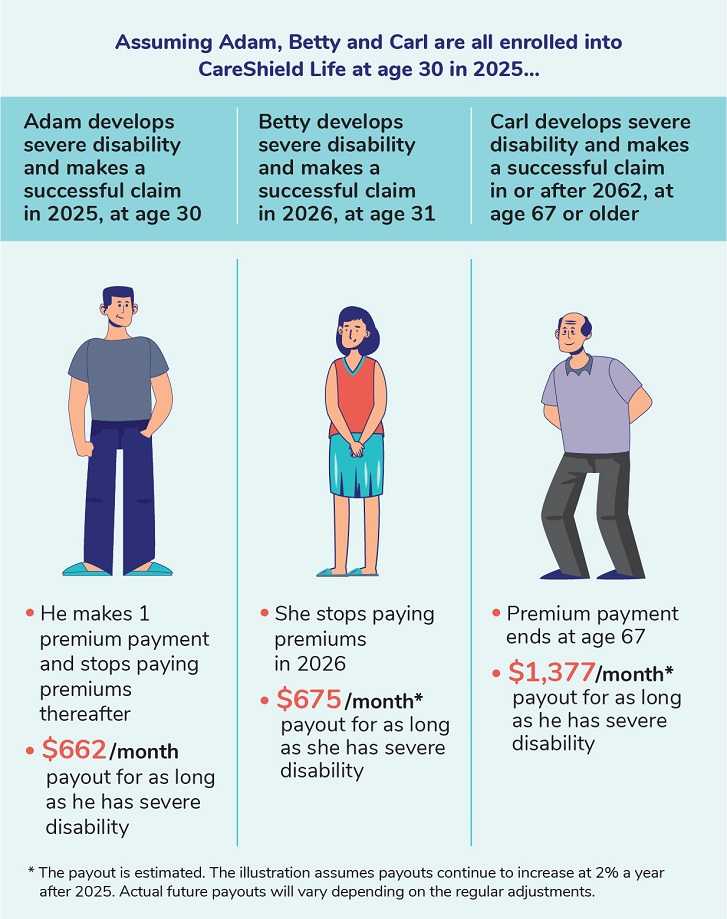

Monthly payout is $662 in 2025, and increases annually until age 67 or when a successful claim is made, whichever is earlier.

For example, if a 30-year-old individual joined CareShield Life in 2020, develops severe disability and makes a claim in 2025, he/she can potentially receive $662 per month, for the entire duration of severe disability. However, if a 30-year-old individual joined CareShield Life in 2020, and develops severe disability at age 67 or later, he/she can potentially receive $1,200 per month upon making a successful claim, for the entire duration of severe disability.

For an insured (born in 1954 and earlier) who joined the scheme at age 67 or after, his/her monthly payout will be fixed at $612/month when a successful claim is made.

2. What will be the rate of premium and payout increment for CareShield Life?

The rate of premium and payout increases for CareShield Life will have to be reviewed regularly based on actuarial principles, taking into account factors like changes in claims experience and longevity. This is important to keep the fund sustainable.

An independent council has been set up to regularly review these trends and advise the Government on premium and payout adjustments in accordance with an actuarially sound adjustment framework. Actual future premiums and monthly payouts will vary depending on the regular adjustments.

To give Singaporeans greater certainty in the first five years, payouts and premiums* will each increase by 2% per year.

*2% increase of premiums per year excludes GST.

3. How was the starting payout of $600 per month for CareShield Life decided?

Long-term care costs vary depending on one’s care needs and arrangements. How one finances these costs also vary, depending on one’s financial resources.

In deciding the enhanced payouts, the ElderShield Review Committee took into account the basic long-term care costs for a range of services and settings, other sources of long-term care funding, such as Government subsidies and assistance schemes, community support, personal savings, family support and Government-funded safety nets e.g. MediFund or ComCare; as well as the need to balance benefits and premium affordability. As part of the overall enhancements to long-term care financing, CareShield Life will provide better protection and assurance to Singaporeans for their basic long-term care needs.

If you wish to have additional coverage, you may consider supplementing your basic CareShield Life insurance with Supplements from the private insurers.

4. Why do CareShield Life payouts stop increasing once insureds stop paying premiums e.g. when they make a claim or turn 67?

CareShield Life payout increases will need to be supported by premium adjustments, to keep the scheme sustainable. Those who wish to have payouts that increase for life may opt to purchase Supplements. Insurers may also wish to take note of CareShield Life features when designing Supplements.

CareShield Life payouts should also not be seen in isolation, but complement existing Government subsidies, Government assistance schemes, community support, personal savings and family support, to better assist Singaporeans with their basic long-term care costs. They can also make monthly cash withdrawals of up to $200 from their and/or their spouse’s MediSave Account(s) under MediSave Care.

For Singaporeans who are unable to pay for their care even after Government subsidies, CareShield Life payouts and personal savings, there are Government-funded safety nets such as MediFund or ComCare which can provide further assistance.

5. As a pensioner, can I receive any special benefits under CareShield Life?

There are no special benefits for pensioners under CareShield Life. Participation in CareShield Life is optional for you, and you can join CareShield Life if you do not develop severe disability. If you are interested in CareShield Life, you may access the CareShield Life Premium Checker e-Service with your Singpass for information on your personalised premiums and premium support.

6. CareShield Life is still targeted at those with severe disability i.e. unable to perform three or more Activities of Daily Living. Why was this retained?

CareShield Life is targeted at severe disability, so that premiums can be kept affordable for all insureds.

If you are a Singaporean with mild or moderate disabilities, and need long-term care, you can tap on means-tested Government subsidies for long-term care services, as well as other Government assistance schemes (e.g. the Seniors’ Mobility and Enabling Fund) to complement your personal savings and family support.

Government-funded safety nets such as MediFund/ComCare can also help you pay for these long-term care costs, should you be unable to afford long-term care services.

If you wish to cover yourself for less severe disabilities, you can consider purchasing Supplements from the private insurers.

7. Why not allow insureds to choose from different CareShield Life plans depending on their ability to pay?

CareShield Life is intended to provide better protection for basic long-term care needs, when payouts are taken together with other long-term care financing sources.

If you wish to have additional coverage beyond what CareShield Life provides, you can consider purchasing Supplements from private insurers.

8. Why can’t CareShield Life automatically reimburse long-term care costs like MediShield Life does for hospital bills?

Monthly cash payouts under CareShield Life will provide more flexibility for individuals with severe disability and their caregivers to decide on their desired care arrangements. This is to ensure that they are not limited to certain long-term care services to be eligible to claim.

For example, some individuals may prefer to remain in a familiar home setting and thus opt for home-based care, while others may prefer receiving care from a healthcare provider such as a nursing home.

9. Can there be lump sum payouts/death benefits/“No-claim Bonus” to incentivise healthy living/two Activities of Daily Living (ADLs) criteria for CareShield Life?

CareShield Life is designed to provide basic financial protection against long-term care costs through monthly cash payouts to insureds with severe disability to cover their ongoing costs. It is not designed or priced to cover payouts if insureds remain healthy.

If you wish to obtain additional coverage including lump sum payouts and death benefits, you can consider purchasing Supplements from the private insurers.

10. Will my CareShield Life be terminated if I am no longer a Singapore Citizen or Permanent Resident?

CareShield Life is intended to be a universal long-term care insurance scheme and part of Singapore’s social safety net for Singapore Citizens and Permanent Residents. Those who renounce their Singapore Citizenship or Permanent Resident status will lose their CareShield Life cover.

This approach differs from ElderShield scheme as ElderShield is not a universal scheme, and there is no Government support provided in the form of premium subsidies and incentives.

-

1. What Government subsidies or incentives are available to help me with my CareShield Life premiums?

To ensure that CareShield Life premiums are affordable, the Government provides means-tested premium subsidies of up to 30% of premiums of CareShield Life, to help lower- to middle-income households.

The Government also provides Additional Premium Support for Singaporeans who are unable to pay their CareShield Life premiums even after premium subsidies.

For more information on the types of premium support available, you may refer to this page. For information on your personalised premiums and premium support, you may access the CareShield Life Premium Checker e-Service with your Singpass.

2. Why do CareShield Life premiums increase over time?

Annual increases in CareShield Life payouts help protect the value of CareShield Life payouts over time. This needs to be supported by annual increases in CareShield Life premiums. To give Singaporeans greater certainty in the first five years, payouts and premiums* will each increase by 2% per year.

An independent council will be set up to regularly review these trends and advise the Government on CareShield Life premium and payout adjustments in accordance with an actuarially sound adjustment framework. The Government will consider affordability of premiums when reviewing the council’s advice on premium adjustments.

*2% increase of premiums per year excludes GST.

3. Are the increases in CareShield Life payouts and premiums fixed at 2% annually?

To provide greater assurance to Singaporeans, for the first five years of scheme implementation, payouts and premiums* will both increase by 2% per year.

*2% increase of premiums per year excludes GST.

4. How often will the CareShield Life premiums increase?

To give Singaporeans greater certainty in the first five years, payouts and premiums* for CareShield Life will each increase by 2% per year.

An independent council will be set up to regularly review these trends and advise the Government on CareShield Life premium and payout adjustments in accordance with an actuarially sound adjustment framework. The Government will consider affordability of premiums when reviewing the council’s advice on premium adjustments.

*2% increase of premiums per year excludes GST.

5. What will be the CareShield Life premiums when a 30-year-old today reaches 67 years old?

For those born in 1980 or later, starting premiums vary by joining age and sex. CareShield Life premiums are designed to increase regularly to support the regular increase in payouts. The schedule of premium increases is not fixed, and will be regularly reviewed by an independent council to ensure the sustainability of the scheme.

As an illustration, for a 30-year-old who joins the CareShield Life scheme upon its launch, his premiums would increase from $17/month to $36/month when he reaches 67 years old, assuming a non-guaranteed 2% premium increase per annum (excluding GST). His payouts would have correspondingly increased from $600/month at scheme launch to around $1,200/month. Actual future premiums and payouts will vary depending on the adjustment each year.

However, to provide greater assurance to Singaporeans, for the first five years of scheme implementation, payouts and premiums* will both increase by 2% per year. An independent council will be set up to regularly review these trends thereafter and advise the Government on premium and payout adjustments in accordance with an actuarially sound adjustment framework.

*2% increase of premiums per year excludes GST.6. I am born in 1979 or earlier. What are my CareShield Life premiums?

You may wish to refer to the CareShield Life Premium Checker e-Service to view your premium details and premium support.

For those born in 1979 or earlier, your premium may have two components:

1. Base premium

All those born in 1979 or earlier and who join CareShield Life will pay a base premium. Base premiums are paid from the age you join until age 67, or for a period of 10 years for those who join at age 59 or older from 6 November 2021.

ElderShield 400 insureds who have been consistently on the scheme will only need to pay the base premium component if they join CareShield Life by 31 December 2021.

Base premiums are designed to increase regularly to support the regular increase in payouts but will remain flat after age 67 if they remain payable. From 2020 to 2025, the increase is 2% per year (excluding GST). Beyond that, premium and payout adjustments will be recommended by an independent CareShield Life Council, in accordance with an actuarially sound adjustment framework.

2. Catch-up Component

You will need to pay a catch-up component, on top of the base premium, if:

i. You are an existing ElderShield 300 insured.

ii. You are not insured under ElderShield or have opted into ElderShield late.

iii. You are an existing ElderShield 400 insured who joined CareShield Life later (from 1 January 2022 onwards).

iv. Your ElderShield 300/400 policies have become reduced paid-up (i.e. you stopped paying premiums after a minimum number of years of premium payment, which qualifies you for a lower payout amount).This is because you would not have paid as much premiums as those in the same cohort who had been consistently insured under the ElderShield 400 scheme and joined CareShield Life earlier.

The catch-up component will also be applicable to foreigners who become Singapore Citizens/Permanent Residents from 1 October 2020 onwards.

The catch-up component is a flat amount paid over across 10 years and is paid on top of the base premium.

7. I am born in 1979 or earlier. Will the premiums I had already paid under ElderShield be taken into account when I join CareShield Life?

ElderShield premiums that ElderShield 300/400 insureds have already paid will be taken into account when computing their CareShield Life premiums. ElderShield Supplement premiums will not be taken into account when computing CareShield Life premiums. ElderShield Supplements provide coverage beyond ElderShield, and their benefits will continue to be recognised even if an ElderShield insured upgrades to CareShield Life, as long as the insured continues paying his Supplement premiums and does not terminate his Supplement coverage.

8. I am born in 1979 or earlier. Can I choose to receive the CareShield Life participation incentive as one lump sum?

The participation incentive was offered to encourage Singapore Citizens born in 1979 or earlier to join CareShield Life by helping to offset the annual premiums payable. As such, the Government has designed it to be spread over 10 years of premium payment.

Participation incentive is only provided to Singapore Citizens who joined and were covered under CareShield Life by 31 December 2024.

9. What is the catch-up component under CareShield Life?

All Singapore residents born in 1979 or earlier who join CareShield Life will pay a base premium.

If you are an existing ElderShield 400 insured who have been consistently on an ElderShield policy (i.e. never opted out, or upgraded from ElderShield 300 to ElderShield 400 in 2007 when you had the chance to) and join CareShield Life by 31 December 2021, you will only pay the base premium each year.

You will need to pay a catch-up component, on top of the base premium, if:

i. You are an existing ElderShield 300 insured.

ii. You are not insured under ElderShield or have opted into ElderShield late.

iii. You are an existing ElderShield 400 insured who joined CareShield Life later (from 1 January 2022 onwards).

iv. Your ElderShield 300/400 policies have become reduced paid-up (i.e. you stopped paying premiums after a minimum number of years of premium payment, which qualifies you for a lower payout amount).This is because you would not have paid as much premiums as those in the same cohort who are covered under the ElderShield 400 scheme and joined CareShield Life earlier. The catch-up component will be paid over 10 years and will remain a flat amount.

The catch-up component will also be applicable to foreigners who become Singapore Citizens/Permanent Residents from 1 October 2020 onwards.

10. I am born in 1979 or earlier. Why are there no subsidies for the catch-up component when it looks so substantial?

All Singapore Citizens and Permanent Residents born in 1979 or earlier who join CareShield Life will pay a base premium that takes into account the premiums existing ElderShield 400 insureds in their cohort have already paid for ElderShield.

You will need to pay a catch-up component, on top of the base premium, if:

i. You are an existing ElderShield 300 insured.

ii. You are not insured under ElderShield or have opted into ElderShield late.

iii. You are an existing ElderShield 400 insured who joined CareShield Life later (from 1 January 2022 onwards).

iv. Your ElderShield 300/400 policies have become reduced paid-up (i.e. you stopped paying premiums after a minimum number of years of premium payment, which qualifies you for a lower payout amount).The catch-up component will also be applicable to foreigners who become Singapore Citizens/Permanent Residents from 1 October 2020 onwards.

The catch-up component is not subsidised to ensure parity in premium subsidies across different groups within those born in 1979 or earlier.

Nonetheless, for those who are unable to pay for their CareShield Life premiums even after premium subsidies, the Government will provide Additional Premium Support.

11. Do the MediSave contribution rates need to be increased because of the higher CareShield Life premiums?

The current MediSave contribution rates already allow most working households to pay for CareShield Life and MediShield Life premiums from their monthly MediSave contributions. The Government will continually review the MediSave contribution rates to ensure that they are adequate for the future healthcare needs of Singaporeans.

12. What are my premiums when I enrol in CareShield Life?

You may wish to refer to the CareShield Life Premium Checker e-Service to view your premium details and premium support.

13. Why was the CareShield Life premium payment term extended to age 67?

Starting the CareShield Life premium payment duration at age 30, and ending at age 67 lengthens the premium payment duration. A longer duration of premium payment allows insureds to spread premium payment over more years, so as to reduce annual premiums payable.

The premium payment end age might be subsequently reviewed to take into consideration the changes in the re-employment age. Ample notice will be given to cohorts who are affected by any changes to the premium payment end age.

14. When can I expect more information on my CareShield Life premiums so I can make a decision?

You may wish to refer to the CareShield Life Premium Checker e-Service to view your premium details and premium support.

15. Will the CareShield Life premium payment end age go up further based on the prevailing re-employment age?

The premium payment end age of CareShield Life will be set taking into account any changes to the re-employment age in future. Ample notice will be given to you if you are affected by any changes to the premium payment end age.

16. Why are CareShield Life premiums for older cohorts higher than younger cohorts?

The estimated premiums for all cohorts are actuarially determined and are designed to be not-for-profit.

CareShield Life premiums are meant to be paid from age 30 to 67, or until the insured makes a claim. Older cohorts joining CareShield Life will face higher annual premiums as they have fewer years to spread their premium payments as compared to younger cohorts. Older cohorts also have a higher risk of developing severe disability.

The Government will provide premium support for those born 1979 or earlier:

1. Lower- to middle-income Singapore residents will receive Means-tested Subsidies. Up to two-thirds of Singapore resident households will be eligible for CareShield Life subsidies of up to 30%.

2. Singapore Citizens born in 1979 or earlier will receive Participation Incentives, spread over the first 10 years of their policy if they joined and were covered under CareShield Life by 31 December 2024.

3. Those in financial need who are unable to pay for their premiums after premium subsidies can apply for Additional Premium Support from the Government.

For more information on the types of premium support available, you may refer to this page. For information on your personalised premiums and premium support, you may access the CareShield Life Premium Checker e-Service with your Singpass.

17. Why are CareShield Life premiums for females higher although their payouts are the same as males?

CareShield Life provides the same amount of expected benefits per dollar of premium paid for both women and men over their lifetimes. Compared to men, women generally live longer and have higher chances of developing severe disability, hence they are likely to receive longer CareShield Life coverage and more payouts over their lifetime. As men and women pay premiums for CareShield Life for the same number of years, the annual premiums for women need to be higher to account for their longer expected duration of payout over their lifetime.

We will provide support to lower-income women through the existing social support schemes for lower-income Singaporeans. For CareShield Life, the Government will also provide premium subsidies and support based on one’s financial circumstances to ensure that premiums are affordable.

18. Why not extend premium payment for life for CareShield Life, like MediShield Life?

Lengthening the premium payment duration by bringing down the start age to age 30 and extending the end age to 67 is sufficient to improve CareShield Life premium affordability, while still keeping premium payment largely during one’s working years.

19. What if CareShield Life premiums result in me not meeting the Basic Healthcare Sum (BHS)?

The Basic Healthcare Sum (BHS) is an estimate of what you need for your basic subsidised healthcare expenses in old age. As CareShield Life premium payments will stop at the re-employment age of 67 for most Singaporeans, the Government does not expect premiums to have a significant impact on the BHS.

While you are not required to top up your MediSave if you do not meet the BHS, you and your family members are strongly encouraged to consider doing so.

20. Does the Basic Healthcare Sum need to be increased because of the higher CareShield Life premiums?

The Basic Healthcare Sum (BHS) is the estimated savings required for basic subsidised healthcare needs in old age. As CareShield Life premium payments will stop at the re-employment age of 67 for most Singaporeans, the Government does not expect premiums to have a significant impact on the BHS.

Nevertheless, the Government will review and adjust the BHS regularly to ensure that Singaporeans’ MediSave savings keep pace with growth in MediSave use by the elderly, especially with rising healthcare costs and expansions in MediSave uses.

21. How will Singaporeans’ eligibility for CareShield Life means-tested premium subsidies be assessed?

Means-tested premium subsidies will depend on Singaporeans’ household per capita income, the annual value of his or her residence, and the number of properties owned. Lower- and lower-middle income Singaporeans who own no more than one property and live in residences with annual values up to $31,000 will be eligible for means-tested premium subsidies.

22. What is the difference in treatment between Singapore Citizens and Permanent Residents for CareShield Life premium subsidies?

For means-tested CareShield Life premium subsidies, Permanent Residents will receive half the means-tested premium subsidy rates applicable to Singapore Citizens, in line with MediShield Life.

23. If I am self-employed/retired/become unemployed before age 67, will I be able to afford CareShield Life premiums?

The Government will provide CareShield Life premium subsidies for lower- and middle-income insureds. Singaporeans who are unable to afford premiums even after premium subsidies can be assisted by Additional Premium Support. No one will lose coverage due to financial difficulties.

24. What will happen to my CareShield Life premiums that I paid should I pass away before claiming?

There is no death benefit for CareShield Life. As such, there will be no payouts upon insureds' passing. If you wish to obtain insurance that provides death benefits, you may purchase Supplements that provide this option.

25. I am covered under CareShield Life. What is Additional Premium Support and who can qualify?

Additional Premium Support (APS) is designed to help Singaporeans who cannot afford CareShield Life/MediShield Life premiums even after premium subsidies and payment by MediSave and have insufficient family support to rely on.